2.1 Winners and losers from Agrarian Reform: Evidence from Danish land inequality 1682–1895

Boberg-Fazlić, N., Lampe, M., Lasheras, P. M., & Sharp, P. (2022). Winners and losers from Agrarian Reform: Evidence from Danish land inequality 1682–1895. Journal of Development Economics, 155, 102813. https://doi.org/10.1016/j.jdeveco.2021.102813

[Link to the full original replication package paper on OSF]

Highlights

The paper examines the distributional effects of land reforms between 1682-1895 in Denmark.

The authors use an Instrumental Variable (IV) to deal with endogeneity issues stemming from reverse causality between the variable of interest (land productivity) and the dependent variable (land inequalities).

This methodology is standard by the choice of a geological instrument. It follows the usual steps of the IV procedure, including tests of the instrument’s pertinence (F-statistic of the 1st stage estimation).

Our added value to the original replication package lies mainly in the detailed explanation of the provided code. Additionally, we show how to extract various tables and figures directly from the Stata code.

We explain these Stata tricks:

Diagnostic Statistics: We leverage the

estat firststagecommand to obtain diagnostic statistics pertaining to the first-stage of instrumental variable estimation, which includes extracting and storing the F-statistics for further analysis.Looping: The

foreachloop structure is used, which enables the iteration over multiple years for instrumental variable regressions and allows to avoid repetitive commands in the code.Advanced Formatting: Through the utilization of the

esttabcommand along with various formatting options, we create well-formatted tables, which results in the production of tables that are not only clear and organized but also visually appealing.

2.1.1 Introduction

As a rule, agrarian reforms are viewed as fundamental for economic development, allowing, on one hand, to fuel agricultural productivity and on the other, to reallocate the necessary productive resources to industrialization. Their design has to fulfill two competing objectives: stimulating farms’ productivity and ensuring an equitable access to land. As numerous reforms have been criticized for failing the latter, this paper provides the first quantitative long-term assessment of the Danish agrarian reforms’ effects on both economic efficiency and land inequalities.

To do so, the authors combine several sources of historical data on farms at the parish level with population and agricultural censuses to cover the 1682-1895 period.

First, they document that the agrarian reform happened between 1784 and 1810, with a unification of property rights, favoring middle-sized farms.

Then, they get the number and sizes of farms per parish for the years 1682, 1834, 1850, 1860, 1873, 1885 and 1895 from Danish land registers, as well as their productive capacity measured in units of barrel of hard grain (HK), which was the unified measure used for tax collection.

Thanks to this data, they can calculate a measure for inequality within parishes for the several data points (their explained variable). They opt for the use of the Theil index to measure land inequality due to its analytically desirable properties. One key advantage is that the Theil index adheres to the principle of transfers, ensuring that a redistribution from one individual to a less affluent one results in a proportional decline in the Theil index, which is particularly convenient for focusing on changes in inequalities over time. Moreover, the Theil index provides unambiguous rankings of distributions, ensuring that two regions with identical Theil indices exhibit identical income distributions (not guaranteed by other common measures such as the Gini index). If a parish have all farms of equal productive size, then its Theil index is 0 ; if only one farm holds all land, its Theil index is the logarithm of the number of households living in the parish.

Finally, they consider the natural logarithm of the total value of the land (measured in HK) of parish p as their main explanatory variable.

Recall that their objective is to estimate the effect of productive capacity on inequality. From an econometric point of view, the most obvious approach would be to regress changes in parish-level land inequalities on a measure of soil productivity. Nonetheless, such a specification would be exposed to endogeneity issues, due to the reverse causality between the explained variable (evolution in land inequalities) and the variable of interest (land productivity): as higher agricultural productivity leads to Malthusian dynamics, in parishes with more fertile soils, there would be more smallholders and landless individuals, whose socio-economic status would then be deteriorated by the reforms. Consequently, areas with a higher agricultural productivity were more exposed to rises in land inequalities. At the same time, population growth has beneficial effects on innovation and thus, agricultural productivity. To tackle this, the authors adopt an IV strategy and choose as an instrument for land productivity the distribution of “Boulder Clay”, the sediment type most adapted to barley, resulting from the Weichselian glaciation. Geological variables are generally viewed as reliable instruments, since they capture long-term determinants of development that are independent from human factors. So their IV is the share of parish area classified as boulder clay (invariant in time).

2.1.2 Identification strategy

When deciding to use a 2SLS strategy, several points need to be discussed in order to allow the identification of robust causal effects. The first hypothesis to be considered and which cannot be tested statistically is the exclusion restriction. It is necessary to rule out any direct effect of the instrument (boulder-clay) on the dependent variable (land inequalities). In this specific case, it can be assumed that soil composition doesn’t directly affect the level of land inequalities. In fact, the authors argue that the rise of inequalities is driven by a stronger demographic growth, due to the productive capacity of the land. This implies, beside the soil fertility, adequate land management practices and efficient agricultural technologies. The authors also have to exclude any effect of the dependent variable on the instrument. Here, once again, land inequalities and the soil fertility seem to be unrelated, as the soil’s share of boulder clay stems from the Weichselian glaciation, which occurred approximately 18,000 years ago. Moreover, the sediment classification they use was made below the impact area of cultivation practices and technologies, which allows to infirm a potential effect of inequalities on this measure of land fertility.

The second hypothesis to be respected is the instrument’s relevance.

The authors need to convincingly describe how the instrument affects the

endogenous variable. In our case, the soil composition represents a key

determinant of the land’s productivity and thus is supposed to be

positively correlated with the total production of an area measured by

the variable TotalHK. Unlike the aforementioned exclusion restriction,

this assumption can be tested statistically. It can be done, for

instance, by verifying whether after estimating the first-stage

specification (1), the coefficient of the instrumental variable is

statistically significant or whether the F-statistic is superior to the

conventionally fixed value of 10.

\[\begin{equation} \tag{1} ln(TotalHK)_{p}=α_{0}+βBoulderClay_{p}+λ_{r}+X_{p}γ+ϵ_{p} \end{equation}\]

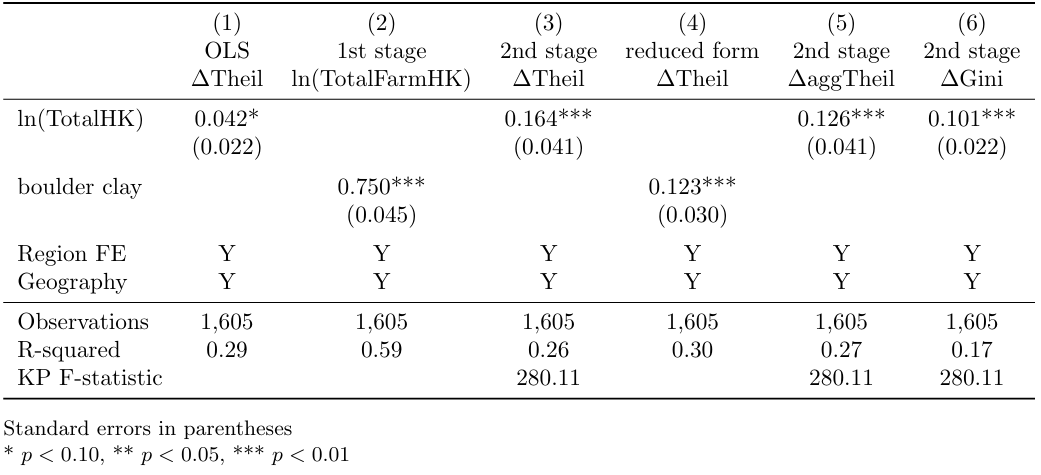

As we can see in column 2 of Table 1, the effect of the soil composition

on total production is statistically significant at 1% level. Also, the

value of the F-statistic is equal to 280. Hence, we can conclude that

both steps necessary to ensure the relevance and the exogeneity of the

instrument have been fulfilled. That said, they further estimate the

second-stage specification (2).

\[\begin{equation} \tag{2} ΔTheil_{p}=α_{0}+β\widehat{ln(TotalHK)}_{p}+λ_{r}+X_{p}γ+ϵ_{p} \end{equation}\]

After estimating both the OLS and the second-stage IV specifications, the authors find statistically significant positive effects of land productivity on land inequalities during the agrarian reforms. To ascertain the robustness of these findings, they estimate additional specifications, using alternative measures of land inequalities – such as Gini index, an alternative to the Theil index – and of land productivity – the amount of barley paid in tax. As no significant change in the results was detected, we can conclude that the econometric estimation allowed them to confirm their predictions, exposed in the theoretical part of the paper. In the next part of our narrative, we will discuss some of the main figures of the paper. We will also indicate the necessary commands to replicate them using Stata.

2.1.3 From the article to practice: exploring the replication code

2.1.3.1 Getting started: database access and required packages

In order to open the Stata database and execute the following lines of

code, several packages need to be downloaded and installed. In this

section, we guide you through the process of accessing the database and

briefly refer to these packages. In what follows, you have to download the original dataset from a link, then run these first lines of code to get the shorter version of the dataset, for which we also provide you with a codebook (see header).

***Open the database***

*download and save WinnersandLosers_finaldata.dta from: https://osf.io/jmn5y/files/osfstorage?view_only=f18f6d51efe44f04abef6e9042c0163c

*define your working directeory, where you also just stored the dataset

cd "C:\Users\" /*C:\Users\ = path where you also store the dataset*/

use "WinnersandLosers_finaldata.dta", clear

keep ID BygLG Lat Long year MLmean Theil_c AggTheil_c gini1682 gini1834 region ln_area LnDistCoast LnDistCPH ln_TotalFarmHK ln_Theil_1682c ln_Theil_1834c ln_Theil_1850c ln_Theil_1860c ln_Theil_1873c ln_Theil_1885c ln_Theil_1895c year_1 Gini ln_TotalFarmHK1682 ln_TotalFarmHK1834 ln_TotalFarmHK1850 ln_TotalFarmHK1860 ln_TotalFarmHK1873 ln_TotalFarmHK1885 ln_TotalFarmHK1895 ln_TotalFarmHK1682_nohouses ln_TotalFarmHK1834_nohouses ln_TotalFarmHK1850_nohouses ln_TotalFarmHK1860_nohouses ln_TotalFarmHK1873_nohouses ln_TotalFarmHK1885_nohouses ln_TotalFarmHK1895_nohouses

save "Dataset_AA_ALC_AT.dta", replaceSubsequently, several Stata packages are necessary to execute the

replication code successfully.

The first package needed is the estout package. This package allows

to make regression tables using regressions previously stored in the

Stata memory.

The second package required is the ivreg2 package. This package

allows to run instrumental variables regressions.

The third package is the coefplot package. This package is used to

create coefficients plots which visually represent the estimated

coefficients and their confidence intervals.

The fourth package is outreg2. This package is used to produce

illustrative tables of regression outputs. This package is able to write

LaTex-format tables.

All the packages can be installed using the following lines of code.

Table 1: IV estimation using total HK and the share of parish area classified as boulder clay

***Table 1***

use "Dataset_AA_ALC_AT.dta", clear

***Column (1) : OLS***

eststo ols1: qui reg D.Theil_c ln_TotalFarmHK ln_area LnDistCPH Lat Long LnDistCoast ///

i.region if year==1834, vce(robust)

eststo ols2: qui reg D.AggTheil_c ln_TotalFarmHK ln_area LnDistCPH Lat Long LnDistCoast ///

i.region i.year if year==1834, vce(robust)

***Column (2) : First-stage***

eststo fiv1: qui reg ln_TotalFarmHK MLmean ln_area LnDistCPH Lat Long LnDistCoast ///

i.region if year==1834, vce(robust)

***Column (4) : Reduced form***

eststo ziv1: qui reg D.Theil_c MLmean ln_area LnDistCPH Lat Long LnDistCoast i.region ///

if year==1834, vce(robust)

***Column (3) : Second-stage (with diffTheil)***

eststo ivdiff1: qui ivregress 2sls D.Theil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Column (5) : Second-stage (with diffAggTheil)***

eststo ivdiff2: qui ivregress 2sls D.AggTheil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Column (6) : Second-stage (with Gini)***

eststo ginihkdiff: qui ivregress 2sls D.Gini ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Formation of Table 1***

esttab ols1 fiv1 ivdiff1 ziv1 ivdiff2 ginihkdiff, se star(* 0.10 ** 0.05 *** 0.01) b(3) ///

r2 var(15) model(12) wrap keep(MLmean ln_TotalFarmHK) mtitles("OLS" "first stage" ///

"second stage (diffTheil)" "reduced form (diff Theil)" "second stage (diffAggTheil)" ///

"second stage (diffGini)" ) stats(N r2 Fstat, labels("Observations" "R-squared" ///

"KP F-statistic") fmt(%9.0fc 2 2)) indicate("Region FE = 2.region" ///

"Geography = LnDistCPH" , labels(Y N)) labelOLS regressions by replicating the columns 1,2 and 4 of Table 1

***Table 1***

eststo clear

***Column (1) : OLS***

eststo ols1: qui reg D.Theil_c ln_TotalFarmHK ln_area LnDistCPH Lat Long LnDistCoast ///

i.region if year==1834, vce(robust)

eststo ols2: qui reg D.AggTheil_c ln_TotalFarmHK ln_area LnDistCPH Lat Long LnDistCoast ///

i.region i.year if year==1834, vce(robust)

***Column (2) : First-stage***

eststo fiv1: qui reg ln_TotalFarmHK MLmean ln_area LnDistCPH Lat Long LnDistCoast ///

i.region if year==1834, vce(robust)

***Column (4) : Reduced form***

eststo ziv1: qui reg D.Theil_c MLmean ln_area LnDistCPH Lat Long LnDistCoast i.region ///

if year==1834, vce(robust)Columns 1, 2, and 4 of Table 1 represent two Ordinary Least Squares

(OLS) regressions, a first-stage, and a reduced form, respectively,

representing distinct stages through OLS regressions. These different

model specifications are often used in econometric analyses to examine

causal relationships between variables. These columns offer a

comprehensive understanding of underlying economic relationships and

allow for nuanced interpretation of results. The singular variable

differing across the two OLS regressions is the initial variable,

corresponding to the dependent variable: the change in the Theil index

from 1682 to 1834 D.Theil_c and the change in the Theil index of

1834 aggregated to the size categories of 1682 D.AggTheil_c,

respectively. In line with our approach of conducting both the

first-stage and the reduced form analyses, we introduce the instrumental

variable MLmean in the two last regression equations. The

replication process of these columns involves several crucial steps in

estimating econometric models.

Firstly, the use of the eststo clear command ensures a reset of

previous estimation results, creating a clean environment before running

new estimations. Subsequently, the inclusion of qui – for quietly

– with the reg – for regress – function allows for the temporary

storage of regression results in a named matrix, such as ols1 in the

first model. Moreover, the model specification, denoted as

D.Theil_c ln_TotalFarmHK ln_area LnDistCPH Lat Long LnDistCoast i.region,

details the variables included in the regression equation. It is crucial

to note that this specification is essential for understanding the

relationships between key variables and the dependent variable – here

D.Theil_c or D.AggTheil_c. Furthermore, the use of the

conditional if year==1834 filters the data, retaining only

observations where the year variable is equal to 1834. This

filtering step enables a focus on a particular year – here 1834 –,

allowing for a more targeted analysis. Finally, the vce(robust)

option is specified to estimate robust standard errors, thereby

addressing potential heteroskedasticity issues. These robust standard

errors are particularly important to ensure the reliability of

estimation results, especially when residuals exhibit heterogeneous

variations.

IV regressions by replicating columns 3,5 and 6 of Table 1

***Table 1***

***Column (3) : Second-stage (with diffTheil)***

eststo ivdiff1: qui ivregress 2sls D.Theil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Column (5) : Second-stage (with diffAggTheil)***

eststo ivdiff2: qui ivregress 2sls D.AggTheil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Column (6) : Second-stage (with Gini)***

eststo ginihkdiff: qui ivregress 2sls D.Gini ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4] The columns 3, 5, and 6 which represent second-stages, are estimated

through instrumental variable regressions. Similar to OLS regressions,

the command eststo ivdiff1 : qui is used to store the estimation

results in a matrix named ivdiff1, ensuring an organized storage of

relevant information. Secondly, the function ivregress 2sls is

applied to conduct a two-stage IV regression, as indicated by 2sls.

Additionally, the explanatory variables

D.Theilc lnarea LnDistCPH Lat Long LnDistCoast i.region mirror those

used in the OLS regressions, providing continuity in the model

specification. The only variable differing across each column

specification is the initial variable, corresponding to the dependent

variable : the change in the Theil index from 1682 to 1834 D.Theilc,

the change in the Theil index of 1834 aggregated to the size categories

of 1682 D.AggTheilc, and the change in the Gini coefficient instead

of the Theil index D.Gini, respectively. This nuanced change

reflects the distinct focus on different dependent variables in each

instance, while the remaining explanatory variables remain constant,

allowing for a systematic exploration of the impact of the selected

variables on the varied dependent variables. The inclusion of

(lnTotalFarmHK = MLmean) specifies the endogenous variable

lnTotalFarmHK and its instrument MLmean. This crucial

specification distinguishes the endogenous variable and its

corresponding instrument, a fundamental aspect of instrumental variable

estimation. Furthermore, to address heteroskedasticity and

autocorrelation, the vce(robust) command employs a robust

variance-covariance matrix, ensuring the reliability of standard errors

in the estimation.

The upcoming lines of code that we are about to describe initially

seemed somewhat unclear to us. However, despite the initial ambiguity,

they prove to be valuable and, upon closer examination, are now better

understood. This is why we will take the time to provide a clear

explanation of these lines. First, the line estat firststage is

employed to display statistics from the first-stage of the IV

regression. This step is typically utilized to assess the validity of

instruments and ascertain their suitability for the estimation process.

Secondly, storing the first-stage results in a matrix named ‘fstat’ is

accomplished through the line mat fstat = r(singleresults). This

matrix captures relevant statistics from the first-stage, providing a

comprehensive view of the instrumental variable performance. Finally,

the line estadd scalar Fstat = fstat[1,4] introduces a new scalar

variable, Fstat, into the main regression results. This step allows

to extract the F-statistic from the first-stage matrix fstat and

assigns it to Fstat. The F-statistic is a crucial metric in

instrumental variable regression, serving as a diagnostic tool to assess

the overall validity of the instruments used. A high F-statistic, that

is superior to 10, suggests that the instruments collectively have a

strong explanatory power for the endogenous variable. In summary, these

lines of code are essential for evaluating the quality and relevance of

the instrumental variables employed in the two-stage IV regression.

Formatting Table 1, an additional but optional step

***Table 1***

***Formation of Table 1***

esttab ols1 fiv1 ivdiff1 ziv1 ivdiff2 ginihkdiff, se star(* 0.10 ** 0.05 *** 0.01) b(3) ///

r2 var(15) model(12) wrap keep(MLmean ln_TotalFarmHK) mtitles("OLS" "first stage" ///

"second stage (diffTheil)" "reduced form (diff Theil)" "second stage (diffAggTheil)" ///

"second stage (diffGini)" ) stats(N r2 Fstat, labels("Observations" "R-squared" ///

"KP F-statistic") fmt(%9.0fc 2 2)) indicate("Region FE = 2.region" ///

"Geography = LnDistCPH" , labels(Y N)) labelThe next stage in our analysis involves the creation of a comprehensive

table summarizing the results of the previously conducted regressions.

It is essential to note that this step does not stand alone, rather it

complements the preceding two steps in which variables were defined and

regressions were estimated. The resulting table serves as a visual

representation of the relationships captured in the regression models,

enhancing the interpretability and communicative power of the findings.

First, the command esttab ols1 fiv1 ivdiff1 ziv1 ivdiff2 ginihkdiff

specifies which models to include in the table, incorporating the

Ordinary Least Squares (OLS), first-stage instrumental variable (IV),

and second-stage IV regression results. To enhance the clarity of the

table, additional formatting options are applied. The

se star(* 0.10 ** 0.05 *** 0.01) command displays standard errors

with significance stars, denoting significance levels with asterisks.

Thirdly, the b(3) command allows to limit coefficient estimates to

three decimal places, contributing to a cleaner presentation of results.

Moreover, the inclusion of r2 displays the coefficient of

determination, the R-squared, in the table, providing insights about the

explanatory power of the model. The var(15) option limits the

display of R-squared to 15 decimal places.

Additionally, with model(12), we specify the maximum number of

models to display in the table, accommodating up to 12 different model

specifications. The wrap command facilitates the wrapping of long

variable names onto multiple lines, ensuring readability. The

keep(MLmean lnTotalFarmHK) option selectively includes only the

variables MLmean and lnTotalFarmHK in the table, which are our

instrument and endogenous variables. Furthermore, mtitles() assigns

model titles to each specified model, contributing to a more informative

and organized presentation. The

stats(N r2 Fstat, labels("Observations" "R-squared" "KP F-statistic") fmt(%9.0fc 2 2))

option adds relevant statistics to the table, including the number of

observations (N), the R-squared, and the F-statistic. The

indicate ("Region FE = 2.region" "Geography = LnDistCPH", labels(Y N))

command introduces indicator in a regression model. The first part,

"Region FE = 2.region", includes fixed effects for a specific

region, here denoted as 2, representing Jutland. This accounts for

unobserved variation specific to Jutland. The second part,

"Geography = LnDistCPH", introduces an indicator variable related to

geography. The labels Y and N are assigned to indicate the

presence or absence of fixed effects or controls in each observation,

contributing to the model’s interpretability. This step allows for a

nuanced interpretation of how fixed effects and geographic controls

influence the results. Finally, the label option is appended to the

esttab command, indicating that variable labels should be included

in the table for clarity and precision.

In the replication code provided by the authors, no specific instruction

regarding the exportation of tables has been included. Therefore, we

recommend users to add the command using "NameOfYourTable.tex" right

after the last variable mentioned in esttab, just before the comma

in front of se star, if they intend to export the table in LaTeX

format. Alternatively, users can use the command

using NameOfYourTable.txt", at the same location in the code, if

they prefer the table in a text format. This flexibility allows users to

choose the desired output format for the tables based on their specific

needs.

This last step – which involves the formation of the table – can be

used in the context of other studies to generate a clear and visually

appealing table summarizing regression results. However, it is crucial

to emphasize that this step is not indispensable for obtaining

replication results. The results can be independently observed directly

using the same code without the qui option, starting from reg or

ivreg. This underscores the flexibility of the code, allowing

researchers to directly access and analyze the regression outcomes

without relying on the table generation step. While the table

contributes to a more organized presentation, it is not a prerequisite

for the replication process. Users can tailor their analysis based on

their preferences and requirements before proceeding to this step. The

study relies on an instrumental variable method that can be challenging

to comprehend. Explaining the replication code of Table 1 is deemed

essential for us, as it allows a detailed exploration and validation of

the authors’ instrumental variable approach. This importance is further

underscored by the fact that Table 1 showcases the primary results of

the study. Having elucidated the intricacies of the Table 1 replication

code, we will now transition to describing the replication code for

Figure 5.

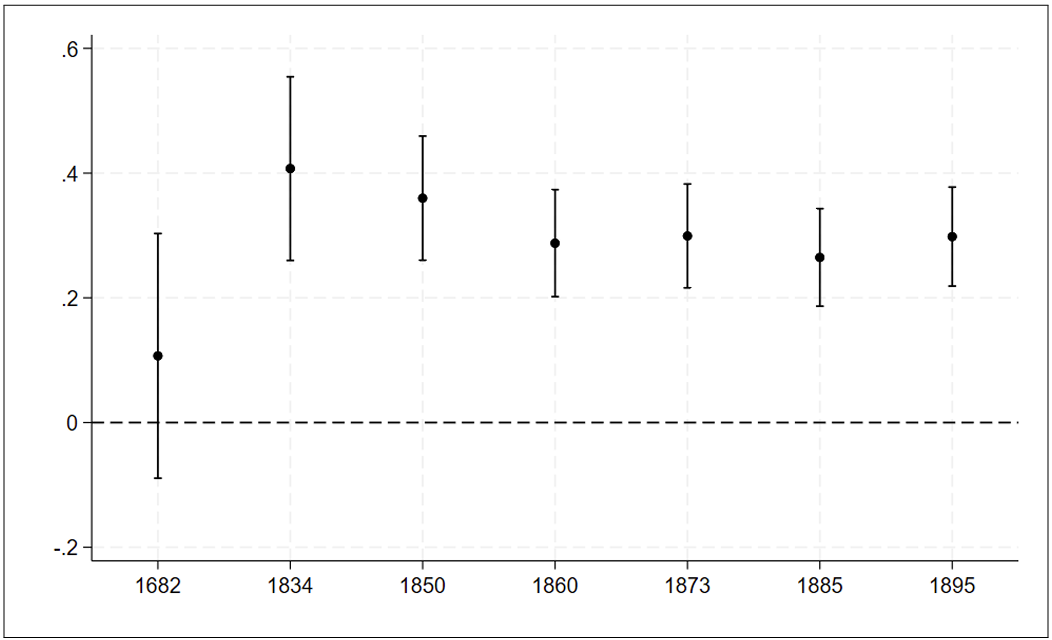

Figure 5

***Figure 5***

eststo clear

foreach x in 1682 1834 1850 1860 1873 1885 1895 {

qui ivregress 2sls ln_Theil_`x'c ln_area LnDistCPH Lat Long LnDistCoast i.region ///

(ln_TotalFarmHK`x' = MLmean) if year==`x', vce(clust ID)

estimates store coef`x'

}

coefplot coef*, vert yline(0) keep(ln_TotalFarmHK*) graphregion(color(white)) ///

ciopts(recast(rcap) lcol(black)) mcolor(black) xtick(1(1)7) ///

xlabel(1 "1682" 2 "1834" 3 "1850" 4 "1860" 5 "1873" 6 "1885" 7 "1895", ) ///

grid(b) legend(off)

graph export "outputfile.png", replaceThe provided Stata code segment serves to illustrate the coefficients

for second-stage estimations conducted over the years 1682 to 1895. The

dependent variable under consideration is ln(Theil), and the

instrumental variable utilized is the share of boulder clay MLmean.

The use of the natural logarithm for the dependent variable

ln(Theil) in the second-stage regression is intentional. This choice

allows for the presentation of estimates for the second-stage

coefficients in levels, offering insight into the relationships over the

years 1682 to 1895. The focus on ln(Theil) in different years

underscores a preference for examining the absolute values of Theil

index rather than changes in Theil index, providing a comprehensive

perspective on the dynamics of the variable across the specified

temporal range.

Initially, eststo clear ensures a clean slate by clearing any

previously stored estimation results. Subsequently, the foreach loop

in the provided Stata code serves as an iterative mechanism, allowing

the execution of specified commands for each value in the specified

range or list. In this case, the loop iterates over the years 1682,

1834, 1850, 1860, 1873, 1885, and 1895. For each iteration, the code

within the loop conducts a 2-stage least squares regression using the

ivregress 2sls command, estimating a model for the given year. The

model includes various independent variables such as

lnTheil’x’c, lnarea, LnDistCPH, Lat, Long, LnDistCoast as

well as the endogenous variable lnTotalFarmHK instrumented by

MLmean and there are fixed effects for region. The purpose of

the loop in this context is to efficiently run the same regression model

for multiple years, automating the process and avoiding redundant code.

This is particularly useful when dealing with time-series data or when

conducting analyses for various time points. The resulting coefficient

plot provides a concise and visual representation of the dynamics of the

variable of interest across different years. The line

estimates store coef’x’ facilitates the storage of estimation

results in matrices named coef’x’, where x represents the

specific year. Following the loop, the coefplot coef* command

generates a coefficient plot based on the stored estimation results,

specifically focusing on coefficients related to the variable

lnTotalFarmHK across the years.

In terms of visual representation, the plot includes a vertical line at

0 for reference with the vert yline(0) command, retains only

coefficients related to lnTotalFarmHK with the

keep(lnTotalFarmHK*) command, and employs a white background for

enhanced clarity thanks to the graphregion(color(white)). Confidence

intervals are displayed using a horizontal line in black with

ciopts(recast(rcap) lcol(black)), and the markers – dots –

representing coefficient estimates are colored black for visibility with

the mcolor(black) option. Additionally, xtick(1(1)7) and

xlabel(1 "1682" 2 "1834" 3 "1850" 4 "1860" 5 "1873" 6 "1885" 7 "1895"),

allow stick marks and corresponding labels on the x-axis to be

strategically positioned to represent each year from 1682 to 1895.

Gridlines are incorporated for ease of interpretation grid(b), and

the legend is turned off for a clean and uncluttered visual

representation thanks to the legend(off) command.

The final line of code, graph export "outputfile.png", replace, is

added by us to the replication code for the purpose of exporting the

coefficient plot as a PNG file. This command utilizes Stata’s graph

export feature, allowing us to save the generated graph to an external

file named “outputfile.png” in the current working directory. The

option "replace" ensures that if a file with the same name already

exists, it will be overwritten. This line of code enhances the

replicability of the study by facilitating the export of the coefficient

plot in a widely used PNG format for further analysis or inclusion in

reports and presentations. This meticulous approach allows for a

comprehensive exploration of coefficient dynamics over time, offering

insights into the relationship between the dependent variable,

ln(Theil), and the instrumental variable MLmean – share of

boulder clay – with controls included, across the specified years. With

the explanation of the coefficient plots for second-stage estimations

complete, our attention now shifts to describing the replication code

for Table A.3 found in the Appendix.

Table 3: Robustness check: Second-stage IV estimates using Gini coefficient

***Table A.3***

***Creation of a loop***

eststo clear

foreach x in 1682 1834 {

eststo ginihk`x': ivregress 2sls gini`x' ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==`x' & gini1834!=., vce(clust ID)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

}

***Formation of Table A.3***

esttab ginihk1682 ginihk1834, se star(* 0.10 ** 0.05 *** 0.01) b(3) r2 var(15) model(11) ///

wrap keep(ln_TotalFarmHK) mtitles("2nd stage: Gini diff" "2nd stage: gini 1682" ///

"2nd stage: gini 1834") stats(N r2 Fstat, labels("Observations" "R-squared" ///

"KP F-statistic") fmt(%9.0fc 2 2)) indicate("Region FE = 2.region" ///

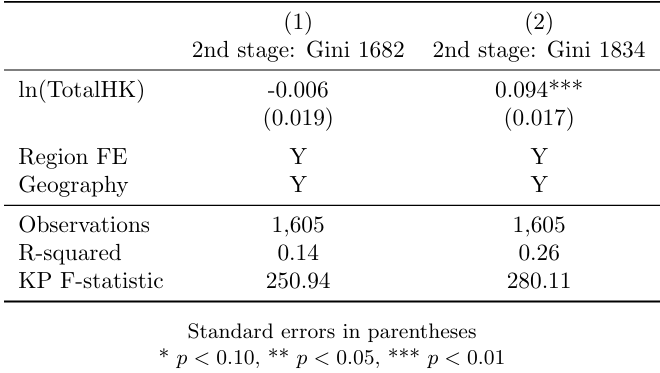

"Geography = LnDistCPH" , labels(Y N)) labelTable A.3 in the Appendix presents robustness check results, specifically second-stage instrumental variable estimates using the Gini coefficient. This additional analysis aims to verify the robustness of the findings by employing an alternative measure. The choice of the Gini coefficient not only enhances interpretability but also provides a basis for comparing and validating the study’s results against a broader scholarly context.

Creation of a loop

***Table A.3***

***Creation of a loop***

eststo clear

foreach x in 1682 1834 {

eststo ginihk`x': ivregress 2sls gini`x' ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (ln_TotalFarmHK = MLmean) if year==`x' & gini1834!=., vce(clust ID)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

}Firstly, the use of the eststo clear command ensures a reset of

previous estimation results, creating a clean environment before running

new estimations. The loop designated by foreach x in 1682 1834

iterates over two specific years, namely 1682 and 1834. This looping

mechanism, as explained in the preceding section – Section 3.3 –,

provides a concise and efficient way to conduct repetitive tasks for

multiple years. The eststo ginihk‘x’ command within the loop

facilitates the storage of results in matrices named ginihk‘x’, with

x representing the current year in each iteration. For a more

comprehensive understanding of the loop creation and its purpose,

referring to the preceding Section 3.3 is recommended. Moreover, the

ivregress 2sls function is employed to conduct a two-stage

instrumental variable (IV) regression. The model’s explanatory variables

include D.Theil_c ln_area LnDistCPH Lat Long LnDistCoast i.region.

In specifying (ln_TotalFarmHK = MLmean), the endogenous variable –

the natural logarithm of the total value of the land measured in barrel

of hard grain of parish – is denoted as ln_TotalFarmHK and its

instrument is identified as MLmean.

To ensure that the analysis includes only observations for the specified

year x where the variable gini1834 is not missing, the condition

if year==x & gini1834!=. is incorporated. Furthermore, the command

vce(clust ID) is used to adjust standard errors in the regression

model, accounting for within-cluster correlation. The code that we will

now describe mirrors the structure found in Table 1. Following this,

estat firststage is employed to display statistics from the

first-stage of the IV regression. This step is crucial for assessing the

validity of instruments. The subsequent lines involve the storage of

first-stage results in a matrix named fstat using the

mat fstat = r(singleresults) command. This matrix captures relevant

statistics from the initial stage, providing insights into the

instrumental variable performance. Finally,

estadd scalar Fstat = fstat[1,4] introduces a new scalar variable

Fstat into the main regression results. This step extracts the

F-statistic from the first-stage matrix fstat and assigns it to

Fstat. For a more comprehensive understanding of the F-statistics

and its purpose, referring to the preceding Section 3.3.2 is

recommended.

Formatting table A.3, an additional but optional step

***Table A.3***

***Formation of Table A.3***

esttab ginihk1682 ginihk1834, se star(* 0.10 ** 0.05 *** 0.01) b(3) r2 var(15) model(11) ///

wrap keep(ln_TotalFarmHK) mtitles("2nd stage: Gini diff" "2nd stage: gini 1682" ///

"2nd stage: gini 1834") stats(N r2 Fstat, labels("Observations" "R-squared" ///

"KP F-statistic") fmt(%9.0fc 2 2)) indicate("Region FE = 2.region" ///

"Geography = LnDistCPH" , labels(Y N)) labelMoving forward in our analysis, we proceed to construct a comprehensive

table that consolidates the outcomes of the earlier regression analyses.

Importantly, it’s crucial to emphasize that this stage is not conducted

in isolation, instead it builds upon the groundwork laid in the

preceding step where variables were defined and regressions within the

loop were executed. The resultant table serves as a visual

representation, effectively summarizing the relationships captured in

the regression models. This approach enhances the interpretability and

communicative power of the analytical findings. The code employed in the

creation of the comprehensive table A.3 aligns with the methodology

elucidated in Section 3.2.3, specifically used for Table 1. Indeed, the

Stata code provided encompasses the construction of a table using the

esttab command, incorporating results from the two-stage

instrumental variable regressions conducted for the years 1682 and 1834.

Thus, the esttab ginihk1682 ginihk1834 line specifies the models

whose results will be included in the table, representing these two

specific years.

To enhance the clarity and readability of the table, several formatting

commands are employed. The se star(* 0.10 ** 0.05 *** 0.01) line

introduces significance stars denoted by asterisks, indicating the

levels of statistical significance. Additionally, b(3) limits the

coefficient estimates to three decimal places. The inclusion of the

coefficient of determination R-squared is facilitated by r2 command,

with var(15) limiting the number of decimals for R-squared to 15

digits. The model(11) command specifies the maximum number of models

displayed in the table, accommodating 11 different models. Moreover, the

wrap command assists in managing long variable names, allowing them

to span multiple lines for improved readability. The

keep(lnTotalFarmHK) line specifies the variable lnTotalFarmHK to

be included in the table. Furthermore, model titles are assigned using

mtitles(), and additional statistics, such as the number of

observations (N), R-squared, and the F-statistic, are incorporated with

stats(N r2 Fstat, labels("Observations" "R-squared" "KP F-statistic")fmt(%9.0fc 2 2)).

The

indicate("Region FE = 2.region" "Geography = LnDistCPH", labels(Y N))

section introduces indicator variables in a regression model. The first

part, "Region FE = 2.region", includes fixed effects for a specific

region, here denoted as 2, representing Jutland. This accounts for

unobserved variation specific to Jutland. The second part,

"Geography = LnDistCPH" introduces an indicator variable related to

geography. The labels Y and N are assigned to indicate the

presence or absence of fixed effects or controls in each observation,

contributing to the model’s interpretability. Finally, the label

option appended to the end of the esttab command ensures that

variable labels are included in the table, enhancing the

interpretability of the presented results.

Once again, in the provided replication code by the authors, no specific

instruction regarding the exportation of tables has been included.

Therefore, we recommend users to add the command

using "NameOfYourTable.tex" right after the last variable mentioned

in esttab, just before the comma in front of se star, if they

intend to export the table in LaTeX format. Alternatively, users can use

the command using NameOfYourTable.txt", at the same location in the

code, if they prefer the table in a text format. This flexibility allows

users to choose the desired output format for the tables based on their

specific needs. This last step to form a table can be employed in the

context of other studies to generate a clear and visually appealing

table summarizing regression results. However, it is crucial to

emphasize that this step is not indispensable for obtaining replication

results.

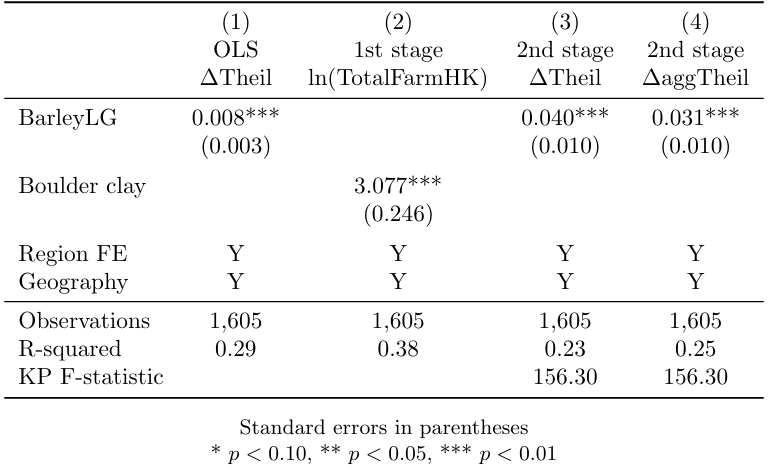

Table 4: IV estimation using barley payments and the share of parish area classified as boulder clay

***Table A.4***

eststo clear

***Column (1) : OLS***

eststo ols1: qui reg D.Theil_c BygLG ln_area LnDistCPH Lat Long LnDistCoast i.region ///

if year==1834, vce(robust)

eststo ols2: qui reg D.AggTheil_c BygLG ln_area LnDistCPH Lat Long LnDistCoast i.region ///

i.year if year==1834, vce(robust)

***Column (2) : First-stage***

eststo fiv1: qui reg BygLG MLmean ln_area LnDistCPH Lat Long LnDistCoast i.region ///

if year==1834 & ln_TotalFarmHK!=., vce(robust)

***Column (3) : Second-stage (diffTheil)***

eststo ivdiff1: qui ivregress 2sls D.Theil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (BygLG = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Column (4) : Second-stage (diffAggTheil)***

eststo ivdiff2: qui ivregress 2sls D.AggTheil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (BygLG = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Formation of Table A.4***

esttab ols1 fiv1 ivdiff1 ivdiff2, se star(* 0.10 ** 0.05 *** 0.01) b(3) r2 var(15) ///

model(11) wrap keep(MLmean BygLG) mtitles("OLS" "first stage" ///

"second stage (diffTheil)" "second stage (diffAggTheil)" ) stats(N r2 Fstat, ///

labels("Observations" "R-squared" "KP F-statistic") fmt(%9.0fc 2 2)) ///

indicate("Region FE = 2.region" "Geography = LnDistCPH" , labels(Y N)) labelTransitioning to another robustness test, presented in Table A.4 in the Appendix, we explore an alternative measure of land quality. In this test, rather than considering the total value of the parish’s HK, the authors focus solely on the amount of barley paid in tax as an indicator of land quality. This measure is derived from the digitization of a map presented by Frandsen in 1988. The results of this robustness check closely resemble the main estimations of table 1, underscoring the consistency and reliability of the analytical findings.

OLS regressions by replicating the columns 1 and 2 of Table A.4

***Table A.4***

eststo clear

***Column (1) : OLS***

eststo ols1: qui reg D.Theil_c BygLG ln_area LnDistCPH Lat Long LnDistCoast i.region ///

if year==1834, vce(robust)

eststo ols2: qui reg D.AggTheil_c BygLG ln_area LnDistCPH Lat Long LnDistCoast i.region ///

i.year if year==1834, vce(robust)

***Column (2) : First-stage***

eststo fiv1: qui reg BygLG MLmean ln_area LnDistCPH Lat Long LnDistCoast i.region ///

if year==1834 & ln_TotalFarmHK!=., vce(robust)In this analysis, we employ familiar Stata commands, akin to those

utilized in Table 1, with the only variable differing across each column

specification is the initial variable, corresponding to the dependent

variable: the change in the Theil index from 1682 to 1834 D.Theilc,

the change in the Theil index of 1834 aggregated to the size categories

of 1682 D.AggTheilc, and the amount of barley paid in tax as an

indicator of land quality BygLG, respectively. In line with our

approach of conducting the first-stage analysis, we introduce the

instrumental variable MLmean to the last regression equation. First,

the command eststo ols1 is used to store the estimation results, and

the results matrix is designated as ols1. The qui function,

signifying quietly, enables the temporary storage of results in the

matrix ols1 for the initial regression. Importantly, this function

ensures that the results of the regression are not displayed at this

point but are preserved under the name ols1 for subsequent

utilization. This approach proves particularly beneficial when authors

later aim to present a comprehensive table with multiple specifications.

Moreover, the reg function is utilized for Ordinary Least Squares

(OLS) estimation, running a regression with specified variables. In this

instance, the regression equation includes Theilc BygLG lnarea

LnDistCPH Lat Long LnDistCoast i.region. A conditional statement,

if year==1834 & lnTotalFarmHK!=., restricts the analysis to

observations where the year variable is equal to 1834, and

lnTotalFarmHK is not missing. This condition ensures a focused

examination of data relevant to the specified year and variable

condition. Furthermore, the use of the conditional if year==1834

filters the data, retaining only observations where the year

variable is equal to 1834. Lastly, the vce(robust) command is

incorporated to specify the use of robust standard errors. This

adjustment is made to account for potential heteroskedasticity and

correlation of errors, enhancing the reliability of the estimation

results.

IV regressions by replicating the columns 3 and 4 of the Table A.4

***Table A.4***

***Column (3) : Second-stage (diffTheil)***

eststo ivdiff1: qui ivregress 2sls D.Theil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (BygLG = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4]

***Column (4) : Second-stage (diffAggTheil)***

eststo ivdiff2: qui ivregress 2sls D.AggTheil_c ln_area LnDistCPH Lat Long LnDistCoast ///

i.region (BygLG = MLmean) if year==1834, vce(robust)

estat firststage

mat fstat = r(singleresults)

estadd scalar Fstat = fstat[1,4] In this specific analysis, we focus on the second-stage of the

estimations with two dependent variables: D.Theilc, representing the

change in the Theil index from 1682 to 1834, D.AggTheilc,

representing the change in the Theil index of 1834 aggregated to the

size categories of 1682. The endogenous variable, the amount of barley

paid in tax as an indicator of land quality BygLG, is instrumented

by the share of boulder clay, utilizing MLmean as the instrumental

variable. This nuanced approach allows us to enhance the robustness of

the estimates and address potential biases in the endogenous variable.

In executing the second-stage of our analysis, employing the

eststo ivdiff1: qui command allows to store the estimation results

in a matrix named ivdiff1. This matrix captures the outcomes of the

two-stage instrumental variable regression facilitated by the

ivregress 2sls command. The regression equation includes explanatory

variables D.Theilc lnarea

LnDistCPH Lat Long LnDistCoast i.region, mirroring the structure of

OLS regressions.

Moreover, the specification (BygLG = MLmean) designates BygLG as

the endogenous variable, with MLmean serving as its instrumental

variable. An instrumentalization that is crucial to address potential

endogeneity concerns and fortifying the validity of the estimations. The

use of the conditional if year==1834 filters the data, retaining

only observations where the year variable is equal to 1834. To

account for heteroskedasticity and autocorrelation, the vce(robust)

command employs a robust variance-covariance matrix. Subsequently, we

encounter the lines of code that initially appeared daunting, but now,

through regular utilization, their functionality has become

comprehensible. Indeed, the estat firststage command is utilized to

display statistics from the first-stage of the IV regression, offering

insights into the validity of the instrumental variables. Further, the

mat fstat = r(singleresults) line stores the first-stage results in

a matrix named fstat, facilitating a comprehensive view of the

instrumental variable performance. Lastly, the

estadd scalar Fstat = fstat[1,4] command introduces a new scalar

variable Fstat into the main regression results. This step extracts

the F-statistic from the first-stage matrix fstat and assigns it to

Once again, for a more comprehensive understanding of the F-statistics

and its purpose, referring to the preceding Section 3.2.2 is

recommended. We would like to remind you that the results can be

independently observed directly using the same code without the qui

option, starting from reg or ivreg. This underscores the

flexibility of the code, allowing researchers to directly access and

analyze the regression outcomes without relying on the table generation

step.

Formatting Table A.4, an additional but optional step

***Table A.4***

***Formation of Table A.4***

esttab ols1 fiv1 ivdiff1 ivdiff2, se star(* 0.10 ** 0.05 *** 0.01) b(3) r2 var(15) ///

model(11) wrap keep(MLmean BygLG) mtitles("OLS" "first stage" ///

"second stage (diffTheil)" "second stage (diffAggTheil)" ) stats(N r2 Fstat, ///

labels("Observations" "R-squared" "KP F-statistic") fmt(%9.0fc 2 2)) ///

indicate("Region FE = 2.region" "Geography = LnDistCPH" , labels(Y N)) labelIn the next step of our analysis, we construct a comprehensive table to

concisely present the findings from our prior regression analyses. It’s

important to emphasize that this stage isn’t isolated but rather

complements the groundwork laid in the preceding steps, where variables

were defined and regressions were conducted. The resultant table serves

as a visual tool to depict the relationships identified in our

regression models, thereby enhancing the clarity and communicative

impact of our analytical insights. In this stage, we use the esttab

command to generate a comprehensive table summarizing the results from

various models, including OLS, first-stage IV, and second-stage IV

regressions. The specified models, denoted as

ols1 fiv1 ivdiff1 ivdiff2, capture different aspects of the

regressions. The se star(* 0.10 ** 0.05 *** 0.01) option is employed

to display standard errors with significance stars, where asterisks

indicate different levels of significance with * for 0.10, ** for

0.05, and *** for 0.01. Setting b(3) limits, once again, the

number of decimal places for coefficient estimates to 3, contributing to

a cleaner presentation.

Including the R-squared r2 and limiting the number of decimals for

the R-squared to 15 digits var(15) provide additional insights into

the explanatory power of the models. Furthermore, the model(11)

option ensures that a maximum of 11 different models is displayed in the

table. To accommodate long variable names, the wrap command is

utilized, allowing for a more organized presentation. Moreover, the

keep(MLmean BygLG) option specifies the variables to be included in

the table, focusing on MLmean and BygLG. Model titles are

designated using the mtitles() option for clarity and organization.

Additional statistics, such as the number of observations (N),

R-squared, and the F-statistic, are included using the

stats(N r2 Fstat, labels("Observations" "R-squared" "KP F-statistic")fmt(%9.0fc 2 2))

option, providing a more comprehensive overview. Moreover, indicator

variables for fixed effects related to a specific region – here 2

representing Jutland – 2.region and geography LnDistCPH are

incorporated using the indicate() option. The labels(Y N))

allows to specify these fixed effects as Y if the fixed effects are

included or as N if they are not This offers further control in

understanding the impact of these factors on the results. Finally, the

label option ensures that variable labels are included in the table,

enhancing the interpretability of the presented information.

Once again, in the provided replication code by the authors, no specific

instruction regarding the exportation of tables has been included.

Therefore, we recommend users to add the command

using "NameOfYourTable.tex" right after the last variable mentioned

in esttab, just before the comma in front of se star, if they

intend to export the table in LaTeX format. Alternatively, users can use

the command using NameOfYourTable.txt", at the same location in the

code, if they prefer the table in a text format. This flexibility allows

users to choose the desired output format for the tables based on their

specific needs.

This last step to form a table can be employed in the context of other

studies to generate a clear and visually appealing table summarizing

regression results. However, it is crucial to emphasize that this step

is not indispensable for obtaining replication results. And although we

conducted a multitude of regressions in Section 3.5.1, it is noteworthy

that the final Table A.4 does not include the ols2 regression.

Finally, the results can be independently used directly with the same

code without the qui option, starting from reg or ivreg.

This highlights the flexibility of the code, allowing researchers to

directly access and analyze the regression outcomes without relying on

the table generation step. While the table contributes to a more

organized presentation, it is not a prerequisite for the replication

process, providing users with the option to tailor their analysis based

on specific preferences and requirements.

Our thorough replication process aimed to transparently convey each step of the analysis, ensuring clarity and reproducibility. We hope that our detailed descriptions provide a comprehensive understanding of the code and methodology employed. Moreover, we hope that this clarity enhances the accessibility of the article and facilitates further examination and validation by other researchers. We trust that transparency is crucial for fostering rigorous and collaborative research practices.

Authors: Auvray Adrien, Carette Anne-Laure, Tarlapan Alina, students in the Master program in Development Economics and Sustainable Development (2023-2024), Sorbonne School of Economics, Université Paris 1 Panthéon Sorbonne.

Date: December 2023